What Happens Behind the Scenes During Failed Paystack Transactions

Introduction

For many customers, a failed Paystack transaction feels straightforward at first. Money disappears temporarily, a checkout page freezes, a debit alert arrives without confirmation, and business owners suddenly begin receiving customer complaints while support tickets start piling up. From the user’s perspective, it appears as though a single payment system simply failed.

Operationally, however, failed transactions are rarely caused by one isolated problem. In many African digital payment environments, a single transaction may quietly depend on multiple interconnected systems functioning correctly at the same time. These systems can include banks, switching infrastructure, mobile networks, card processors, fraud detection layers, merchant APIs, internet connectivity, authentication systems, and reconciliation workflows.

That complexity matters because customers often interpret payment failures emotionally, while payment companies experience them operationally. The difference between those two perspectives explains why failed transactions create so much frustration across African ecommerce ecosystems. What users describe as “Paystack failed” may actually involve delays, interruptions, or coordination problems occurring far outside Paystack’s direct control.

At the same time, businesses still expect payment providers to absorb the emotional consequences of uncertainty. Customers rarely care which institution caused the disruption internally. They simply want clarity, predictability, and reassurance that their money is safe. That tension sits at the center of modern African fintech infrastructure, where trust increasingly depends not only on successful transactions, but also on how platforms manage uncertainty when systems fail behind the scenes.

Understanding what happens during these moments reveals why payment reliability has quietly become one of the most important trust systems in the African digital economy.

Why A Single Online Payment Depends On Multiple Invisible Systems

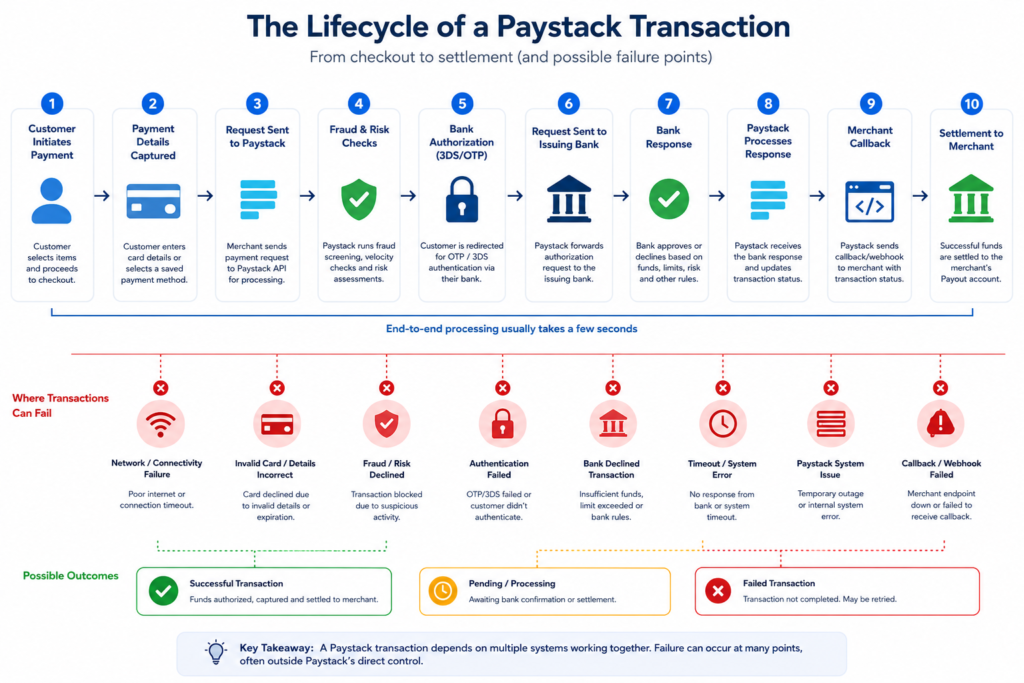

Most users assume online payments move directly from a customer’s bank account into a business account. Operationally, the process is far more layered.

A typical Paystack transaction may involve the customer’s bank, card scheme infrastructure, switching providers, fraud monitoring systems, authentication layers like OTP verification, merchant backend systems, internet connectivity, settlement infrastructure, and reconciliation workflows.

This means a transaction can fail even when Paystack itself is functioning normally.

For example, a customer in Lagos attempts payment during peak evening hours. The merchant website loads slowly because of unstable hosting infrastructure. The customer retries payment multiple times. Meanwhile, the issuing bank experiences temporary latency spikes. The card gets debited, but the payment confirmation fails before the merchant receives verification.

Now three different parties interpret the situation differently. The customer believes money has been taken. The merchant sees no successful payment. The payment processor sees an incomplete transaction state waiting for reconciliation.

This is one reason payment disputes create so much confusion. Different systems may temporarily hold different versions of reality.

Why Failed Transactions Often Increase During High Traffic Periods

One hidden operational reality in African fintech is that infrastructure pressure increases disproportionately Periods like salary payment days, festive shopping periods, betting surges during major football matches, ecommerce sales campaigns, and tuition payment deadlines often create transaction congestion across banking systems during demand spikes.

In many African markets, digital payment adoption has grown faster than infrastructure resilience. That creates a scaling tension fintech operators constantly manage.

Consumers experience digital payments as instant. But behind the scenes, many systems still rely partly on legacy banking architecture not originally designed for massive real-time digital transaction volumes.

This explains why some payment delays appear unpredictable. Operationally, systems may remain technically online while experiencing degraded performance internally.

Transactions begin timing out. Callbacks delay. Authentication slows. Reconciliation queues increase. Customer complaints then rise faster than support teams can respond.

To users, the experience feels chaotic. To operators, it often feels like trying to maintain stability while multiple interconnected systems experience pressure simultaneously.

The Emotional Cost Of Payment Uncertainty Is Larger Than Many Businesses Realize

One failed transaction rarely damages trust by itself. One failed transaction rarely damages trust by itself. Uncertainty does.

Customers can tolerate occasional technical issues when communication feels predictable. What creates anxiety is ambiguity.

For example, a customer receives a debit alert. The merchant says payment was not received. The bank says the transaction is pending. Support channels respond slowly. The customer now experiences a psychological trust gap.

That gap matters because money carries emotional weight, especially across African economies where cash flow pressure is high, disposable income may be limited, informal commerce is common, and financial recovery systems can feel slow or bureaucratic.

In many Nigerian SMEs, a single delayed payment can disrupt inventory restocking, transportation plans, or supplier coordination. For freelancers and small online vendors operating through WhatsApp commerce, failed transactions may temporarily freeze daily operations.

This is why payment reliability affects far more than convenience. It shapes emotional confidence inside digital commerce systems.

Why Reversals Sometimes Take Longer Than Customers Expect

One common misconception is that transaction reversals happen instantly once failure is detected. Operationally, reversals depend on reconciliation processes across multiple institutions.

In some situations, Paystack may already recognize the transaction as failed, while the issuing bank still holds the debit temporarily, or intermediary systems may still be awaiting confirmation signals.

Banks themselves often run reconciliation cycles periodically rather than continuously. This means funds may remain in temporary holding states before automatic reversal occurs.

Where systems coordinate smoothly, reversals happen quickly. Where coordination slows, delays emerge.

This becomes especially complicated when network interruptions occur mid-transaction, customers retry payments repeatedly, authentication partially succeeds, or merchants experience delayed callback confirmations.

Now support teams must investigate transaction trails manually.

And manual reconciliation is one of the least visible but most operationally stressful parts of African fintech infrastructure.

Because customers see only the surface layer. Behind the scenes, teams may be tracing fragmented transaction states across several systems simultaneously.

Why Payment Providers Must Balance Speed Against Fraud Prevention

One operational tension many users never see is the balance between convenience and fraud control. Customers want instant payments, minimal verification, and fast checkout experiences.

But payment providers must also manage fraud attempts, account takeovers, suspicious transaction patterns, stolen card activity, and regulatory compliance obligations.

This creates unavoidable friction.

For example, stricter authentication checks may reduce fraud risk but increase payment abandonment. Meanwhile, faster approval systems may improve customer experience while increasing exposure to fraudulent activity.

In practice, fintech companies constantly make tradeoffs between transaction speed, customer convenience, compliance pressure, fraud prevention, and infrastructure stability.

The challenge becomes even harder across fragmented African banking ecosystems where institutional reliability varies significantly.

Why Merchants Often Experience Payment Failures Differently From Customers

Customers experience failed payments emotionally. Merchants experience them operationally.

For many African ecommerce businesses, payment instability directly affects inventory coordination, order fulfillment, delivery planning, customer support workload, and cash flow predictability.

Imagine an ecommerce business running a promotional campaign. Hundreds of customers attempt checkout simultaneously. Some transactions fail midway. Others succeed without immediate confirmation.

Now the business faces several operational questions:

Should inventory be reserved?

Should delivery processing begin?

Should orders remain pending?

Should customer support intervene manually?

This uncertainty creates invisible coordination costs many customers never see.

Small businesses feel these pressures most severely because they often lack sophisticated finance teams, automated reconciliation systems, or dedicated payment operations staff.

In many African SMEs, founders themselves manually investigate failed payment complaints late into the night.

Why Support Bottlenecks Become More Visible During Payment Problems

One reason payment incidents escalate emotionally is that support systems themselves become overloaded during infrastructure instability.

When payment failures spike, ticket volumes increase, social media complaints rise, merchants demand updates, and customers seek reassurance, while internal operations teams simultaneously investigate system health.

This creates communication lag.

Ironically, users often interpret delayed communication as indifference, even when teams are actively troubleshooting.

Psychologically, silence increases perceived risk, especially in trust-sensitive digital environments.

This is why some fintech companies increasingly prioritize status updates and incident communication even before full resolution occurs. Operational transparency can reduce panic even when technical recovery is still ongoing.

The African Internet Infrastructure Reality Most Users Never Consider

Digital payments depend heavily on stable internet infrastructure. But across many African markets, internet consistency remains uneven.

A transaction may fail because mobile connectivity dropped briefly, a user switched between networks, electricity interruptions affected backend systems, or unstable connectivity interrupted callback communication.

These problems often appear invisible to customers because the payment interface itself still loads.

But transactional infrastructure is highly sensitive to interruption timing.

Even short disruptions during authentication or confirmation stages can create incomplete transaction states.

This explains why fintech infrastructure resilience in Africa involves much more than app design.

It depends on telecom reliability, electricity stability, banking coordination, cloud infrastructure, and institutional interoperability.

Digital payments are ultimately ecosystem systems — not standalone products.

Why Businesses Increasingly Use Multiple Payment Providers

One operational adaptation many African businesses quietly adopt is payment redundancy. Instead of relying entirely on one payment gateway, businesses increasingly integrate multiple providers.

Not necessarily because one platform is “bad.” But because infrastructure unpredictability creates risk concentration.

If one provider experiences temporary disruption, checkout continuity can still continue elsewhere. This reflects a broader operational reality in African digital commerce: Businesses optimize for resilience, not perfection.

Because operators understand that occasional infrastructure instability is sometimes unavoidable.

The real competitive advantage increasingly becomes recovery speed, communication quality, reconciliation efficiency, and customer trust management.

Not merely uptime claims.

Why Payment Reliability Has Become A Competitive Advantage

In the early growth phase of African fintech, convenience drove adoption. Now reliability increasingly shapes loyalty. Customers remember uncertainty more intensely than smooth transactions.

A single unresolved payment dispute can permanently reduce trust in a platform.

This is especially true in African markets where many consumers already carry historical skepticism toward digital financial systems.

Operational predictability therefore becomes psychologically valuable.

Businesses that consistently communicate clearly, resolve disputes quickly, maintain stable infrastructure, and reduce ambiguity often build stronger long-term trust than companies focused purely on rapid expansion.

This shift matters.

Because as African ecommerce ecosystems mature, payment infrastructure is no longer just a technical layer. It is becoming a trust layer for the entire digital economy.

Conclusion

Failed Paystack transactions are rarely just isolated technical incidents. They reveal the hidden complexity behind modern African digital commerce.

Behind every failed transaction may sit fragmented banking infrastructure, overloaded networks, delayed reconciliation systems, fraud prevention controls, support coordination pressure, internet instability, and customer trust sensitivity.

As African digital payments continue scaling rapidly, the real challenge will not simply be processing more transactions. It will be building systems resilient enough to maintain trust during uncertainty.

Because in digital economies, users do not judge platforms only by success rates. They judge them by how predictable, transparent, and recoverable failure feels when things go wrong.

And operationally, that may become one of the most important competitive advantages in African fintech over the next decade.

For more clarity, read:

- Failed Bank Transfers in Nigeria: Causes, Reversals & Solutions

- How To Get Refunds After Failed Transfers

- Cheapest Ways to Receive International Payments in Nigeria

Augustine Tom is the founder and publisher of Brands.Ng, an African business intelligence and digital economy platform covering fintech, ecommerce, logistics, startups, digital platforms, and consumer trust across Africa. He writes about branding, business growth, digital strategy, innovation, and emerging market trends, drawing from experience in business development, consulting, SEO, and digital marketing across diverse industries. His work focuses on analyzing the technologies, systems, and companies shaping Africa’s evolving digital economy.